Why Energy Transition Discourse Needs A Dose Of Realism

Gaurav Sharma, Senior Contributor. Gaurav Sharma is a London-based analyst who covers energy & ESG.

Dec 06, 2025, 06:51am EST

There is growing, even if reluctant, consensus among many experts that the world’s ongoing energy transition, its associated costs, plans, and targets could all do with a heavy dose of realism.

An uncertain macroeconomic climate and a noticeable political blowback against green initiatives in several countries has also knocked the transition trajectory. While BloombergNEF projects the required energy transition investment level to be $5.6 trillion each year from 2025 to 2030, finance is in fact returning unabated to traditional energy if not totally retreating from the green space.

And the spectacular collapse of the Net Zero Banking Alliance in October marked another low point for those seeking to finance the shift from fossil to green fuels. The NZBA counted nearly 150 global banks among its ranks since its founding in 2021. However, mass departures of banks earlier this year dwindled its relevance and ultimately led to its demise.

Major energy companies have also either pulled back or curtailed their green investments, and are placing a renewed overt emphasis on boosting hydrocarbon exploration and revenue.

The topic of tackling the transition took center-stage at the recently concluded Duke of Edinburgh Future Energy Conference in London, U.K., organized by The Worshipful Company of Fuellers, one of the historic livery companies of the City of London, now associated with the whole energy sector.

Interspersed with discussions on renewable energy, oil and gas, hydrogen, geothermal and emerging climate technology solutions, concerns were expressed at the event both about the speed as well as costs and actual efficacy of the transition solutions being proposed.

By Piero Cingari

Published on 09/12/2025 - 7:00 GMT+1

Gold soared over 60% in 2025, driven by geopolitical risks, rate cuts, and central bank demand. Many experts see further upside in 2026, with gold's role as a safe-haven asset still firmly intact.

After a historic 2025 that saw gold soar over 60% and break more than 50 record highs, investors are now turning their attention to whether the precious metal can sustain its upward trajectory into 2026.

Despite leading major asset classes in year-to-date performance, putting it on track for its best year since 1979, experts think gold may still have room to climb next year. Others warn that risks remain.

Unlike previous years when single events dominated gold’s trajectory, this year saw multiple drivers at play.

Sustained central bank buying, persistent geopolitical friction, elevated trade uncertainty, lower interest rates, and a weakening US dollar all combined to fuel demand for the metal as a safe-haven asset.

According to the World Gold Council’s latest report, geopolitical tensions contributed roughly 12 percentage points to year-to-date performance, while dollar weakness and slightly lower interest rates added another 10. Momentum and investor positioning accounted for nine points, with economic expansion contributing a further 10.

Central banks also continued to buy aggressively, keeping official-sector demand well above pre-pandemic norms.

Forecasts from the World Gold Council

Looking ahead, the Council expects many of the forces that powered gold’s extraordinary rally in 2025 to remain relevant in 2026.

However, the starting point is now fundamentally different. Unlike at the beginning of 2025, gold prices have already priced in what the WGC describes as the “macro consensus”. That's expectations of stable global growth, moderate US rate cuts, and a broadly steady dollar.

In this environment, the Council notes that gold appears fairly valued. Real interest rates are no longer falling significantly, opportunity costs are neutral, and the strong positive momentum seen in 2025 has begun to fade.

Investor risk appetite remains balanced, rather than tilting decisively toward caution or exuberance.

As a result, in its baseline scenario, the WGC sees gold trading within a narrow range in 2026, with performance likely limited to between –5% and +5%.

But the outlook is far from settled, as three alternative scenarios could shape a different path.

In a "shallow economic slip" — characterised by softer economic growth and additional Fed rate cuts — gold could rise by 5% to 15% as investors shift toward defensive assets, extending the gains of 2025.

In a deeper economic downturn, or "doom loop," gold could rally by 15% to 30%, fuelled by more aggressive monetary easing, declining Treasury yields, and strong safe-haven flows.

Conversely, if the Trump administration’s policies succeed in reigniting growth, a reflation return would likely push yields and the dollar higher, diminishing gold’s appeal.

Under this bearish scenario, gold could decline by 5% to 20%, particularly if investor positioning reverses and central bank demand weakens.

Predictions from Wall Street

Despite a more measured outlook from the WGC, major investment banks continue to predict further upside for gold in 2026.

J.P. Morgan Private Bank projects prices could reach between $5,200 and $5,300 per ounce, citing strong and sustained demand as a key driver.

Goldman Sachs forecasts gold at around $4,900 per ounce by the end of next year, supported by continued central bank buying.

Deutsche Bank offers a wide range of $3,950 to $4,950, with a base case near $4,450, while Morgan Stanley anticipates prices closer to $4,500, although it warns of near-term volatility.

Supporting this optimism is the ongoing accumulation of gold by central banks, particularly in emerging markets, as well as the view that many institutional investors remain underexposed to the metal.

The potential for lower real yields, coupled with global macro risks, continues to make gold attractive as a portfolio hedge.

Nonetheless, risks could cap further gains. A stronger-than-expected US recovery or a rebound in inflation could force the Federal Reserve to delay or reverse rate cuts, boosting real yields and the dollar, two classic headwinds for gold.

A slowdown in ETF flows or central bank purchases could also dampen demand, while increased recycling, particularly in India where gold is used as collateral, could raise supply and weigh on prices.

A constructive path forward

While a repeat of 2025’s extraordinary 60% surge appears unlikely, gold enters 2026 on solid footing.

The fundamental drivers such as macroeconomic uncertainty, central bank diversification, and gold’s role as a hedge against volatility remain intact.

In a world increasingly defined by unpredictability, gold continues to offer investors not just returns, but resilience. The metal may no longer be in the early stages of a rally, but its role as a strategic anchor in uncertain times is far from diminished.

09 Dec, 2025 By Thomas Johnson

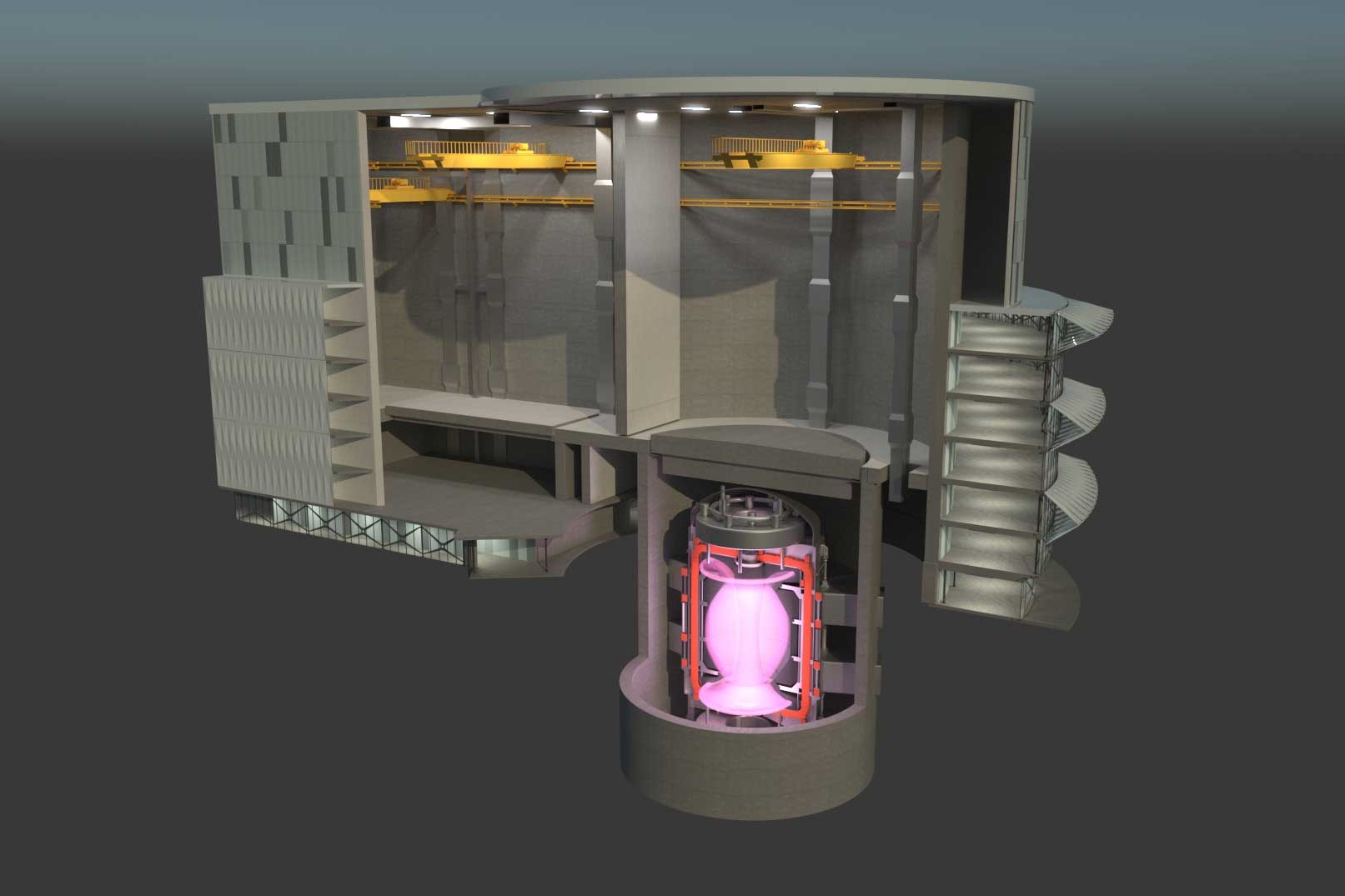

The procurement for an engineering partner to construct the UK’s Spherical Tokamak for Energy Production (Step) fusion power plant will resume “in a year or two” after a failed first attempt, but the choice of a construction partner is imminent.

UK Industrial Fusion Solutions (UKIFS), a subsidiary of the UK Atomic Energy Authority (UKAEA), is leading a public-private partnership to design, build and operate the Step plant. The plant is slated for construction at a West Burton site in Nottinghamshire, chosen for its existing infrastructure (being an ex-coal fired power station) and support from the community for renewed energy generation opportunities.

The government launched a competition to select engineering and construction partners for the prototype fusion energy plant in Nottinghamshire in May last year, with the contracts rumoured to be worth close to £10bn. Then in January, the shortlist for both partners was revealed.

The shortlisted organisations for Step’s engineering partner were:

Engineering procurement hits the wall

Despite announcing the two-consortia shortlist, the project recently divulged that the process of selecting the engineering partner had broken down, with the approach being taken as being deemed “not suitable”.

A statement said: “In the case of the construction partner bidders, the base requirements were understood and UKIFS had confidence that one or more of the bidders’ could meet those requirements. The construction partner procurement will continue to be delivered and is intended to be awarded in line with the expected timescales.

“However, in the case of the engineering partner bidder, it was concluded that the proposed approach was not suitable to take forward at this time.

“The engineering partner element of this procurement process will therefore not proceed to a call for final tenders, and instead UKIFS will procure this capability through other means, primarily through direct engagement with the market.”

Speaking at the Nuclear Industry Association (NIA) annual conference on 4 December, UKIFS chief executive Paul Methven stated procurement for the engineering partner would resume “in a year or two”.

“We’re nearing the final stages of selecting our construction partner in what I have to say has been a really excellent competition,” he said. He said that despite the failed first attempt at procurement, UKIFS will “return to that in a year or two because large scale integration capability is essential for this”.

“In the near term we’re focusing on securing specific support on detailed systems and we’ll have a pipeline of packages coming to market,” he continued. “We’ll be rolling out a pipeline of engineering packages with, hopefully, a significant announcement in March.”

Construction moves ahead

Despite the stumble in procuring an engineering partner, procurement for a construction partner on an equally lucrative deal is on track for decision in the coming months.

The shortlisted organisations for the construction partner are:

The chosen partner is expected to be selected sometime early next year before work on site begins in April.

Methven said: “West Burton operations will move forward really significantly from April, so when our construction partner arrives, we have to be on contract by then to get stuck in into early works.”

Other upcoming movement for the proposed construction of a prototype fusion plant include the launch of Step’s non-statutory public consultation which is due in January and also the Department for Energy Security and Net Zero (DESNZ) is due to update its fusion strategy in March.

Construction of the prototype plant is projected to be completed by 2040.

Trafigura Warns of “Super Glut” as Oil Supply Surges

By ZeroHedge - Dec 10, 2025, 9:00 AM CST

Echoing what has become a now daily refrain by commodity bears everywhere, Saad Rahim, chief economist of commodity-trading giant, Trafigura, said that the oil market faces a “super glut” next year as a burst of new supply collides with weakness in the global economy. According to Rahim, new drilling projects and slowing demand growth would weigh further on already depressed crude prices next year.

“Whether it’s a glut, or a super glut, it’s hard to get away from that,” Rahim said in remarks alongside the company’s annual results.

Brent crude has fallen 16% this year, on track for its worst year since 2020. Prices are expected to be further damped by major projects coming online next year, including in Brazil and Guyana.

The glut thesis is hardly new, and has been popularized by banks such as Citi and Goldman for the past year. As Goldman analyst Daan Struyven wrote in his latest oil tracker note, "global visible oil stocks have built by nearly 2mb/d over the past 30 days." The banks expects them to grow significantly more in the coming years.

Meanwhile, demand from China, which is widely seen as aggressively stocking its strategic petroleum reserve by 500kb/d (and as much as 1 mm/d according to some estimates) and is the world’s biggest oil importer, is expected to grow more slowly next year due to its huge fleet of electric vehicles, which have sharply reduced petrol demand. Low prices this year have prompted China to buy more crude to fill its strategic stockpile.

“China needs to keep buying at this rate, for that super glut to not show up even earlier,” Rahim added.

The US government has also been trying to keep oil prices low, and President Donald Trump has pledged to “drill, baby, drill” in a push to increase American production. There has also been speculation that the US will also refill its SPR which was largely emptied by Biden but since that will promptly drive prices higher, so far this has been nothing but speculation, and meanwhile the US barely has any reserves for a true emergency.

Ben Luckock, head of oil trading at Trafigura, said in October that he expected oil prices could fall below $60 a barrel before rallying. “I suspect we’ll go into the $50s at some point across Christmas and the new year,” he said at the time.

According to the FT, Trafigura reported net profits of $2.7bn during the fiscal year that ended in September, down slightly from $2.8bn the previous year, and a five-year low after years of bumper profits linked to Russia’s full invasion of Ukraine when most commodity traders were breaching sanctions and making a killing in the process.

Its non-ferrous metals trading division reported a record year, due in part to the profits made by shipping copper into the US amid the disruptions caused by whipsawing tariff rules, according to people familiar with the matter.

Trafigura CEO Richard Holtum said “significant headline-driven volatility” had been a major driver for markets this year and that the trend would continue in 2026.

“Trading conditions were not easy last year and our trading team put on a really credible performance across all divisions,” said Holtum.

However, the small drop in profits, combined with rising payouts to Trafigura’s employee-shareholders, meant group equity fell slightly, to $16.2bn, from $16.3bn the previous year, marking the first time this figure has shrunk since 2018.

Payouts to Trafigura’s employees rose to $2.9bn, up from $2bn during the prior year. The company, whose top management is based in Geneva, pays out “dividends” to its employee-shareholders, including by buying back the shares of departing employees over time.

By Zerohedge

https://oilprice.com/Energy/Energy-General/Trafigura-Warns-of-Super-Glut-as-Oil-Supply-Surges.html

Algeria is at a strategic turning point in its economic history, as the country seeks to reduce its dependence on hydrocarbons and build more diversified and sustainable growth. In this context, the mining sector is poised to play a leading role, with the emergence of large-scale, transformative projects capable of reshaping the national production structure. These initiatives are part of a long-term vision aimed at strengthening the country’s sovereignty, developing local industrialization, and creating more skilled jobs.

Focus on Economic Diversification

Algerian authorities present these three projects as the core of their new diversification strategy, directly linking them to the objectives of industrial and agricultural sovereignty and the growth of non-hydrocarbon exports. The government emphasizes the creation of local value through the on-site processing of minerals, in order to replace costly imports and generate foreign currency earnings on international markets.

Gara Djebilet: A Pillar of the Steel Industry

The Gara Djebilet iron ore mine, already in its initial phase of operation, is expected to gradually supply the national steel industry and reduce raw material imports, estimated at several billion dollars annually. By 2030, the associated infrastructure will have a capacity of several million tons of iron ore concentrate and pellets per year, paving the way for Algeria’s greater integration into global metallurgical value chains.

Bled El Hadba: The Fertilizer Bet

The Integrated Phosphate Project, centered on the Bled El Hadba mine in eastern Algeria, aims to produce several million tons of raw phosphate per year and significant volumes of fertilizers for the local market and for export. This complex is presented as a turning point for self-sufficiency in fertilizers and the support of new agricultural areas, with potential revenues in the order of several billion dollars annually and tens of thousands of direct and indirect jobs.

Oued Amizour: Zinc, Lead, and Local Industries

The Oued Amizour-Tala Hamza zinc and lead mine, in the Béjaïa region, is expected to produce hundreds of thousands of tons of zinc and tens of thousands of tons of lead each year. This production is intended to supply local industries (metallurgy, batteries, materials) while generating an exportable surplus, strengthening Algeria’s position in African and Mediterranean markets.

Expected Benefits and Challenges to Monitor

Taken together, these three mega-projects are designed as structuring drivers of growth, thanks to the scale of the investments, the announced jobs, and the projected foreign exchange earnings. Their success will, however, depend on the ability to meet deadlines, secure infrastructure (rail, energy, water) and manage environmental impacts, conditions necessary for economic diversification to be sustainable.

https://www.capmad.com/mining-en/three-mega-mining-projects-are-reshaping-algerias-national-economy/

By Michael Kern - Dec 07, 2025, 4:30 PM CST

The stock market is hitting record highs. GDP growth is in the green. Tech valuations are defying gravity... fueled by a promise that artificial intelligence is going to generate trillions of dollars in wealth.

And yet... everything feels kinda…terrible?

Jobs are disappearing, not in a crash, but in a slow fade. Prices for essentials remain stubbornly high. The divide between the digital economy and physical reality has never been wider.

We are told this is just a transition period. We are told that "efficiency" is messy... but necessary.

But the unease you feel isn’t irrational. The green arrows on the stock charts aren't measuring the health of the everyday economy anymore. They are measuring the success of a takeover.

We are watching a fundamental shift in how the state operates. Sovereignty is shifting from public institutions to a network of private entities. And in many ways, we are holding the door open for them.

When Silicon Valley Bought the State

For years, we talked about the "revolving door" between business and government.

The idea was that regulators would leave office and take cushy jobs at the companies they used to police. It was a conflict of interest... but one we understood.

That metaphor doesn't really fit anymore. This is more like a merger.

A specific network of billionaires and venture capitalists has moved beyond lobbying. They are now building the state infrastructure themselves.

They don't want to influence the rules. They want to be the ones writing the code that executes the rules.

Look at the players involved...

These aren't just businessmen. They are state-builders.

And they’ve spent the last decade funding a pipeline of personnel to place into key government positions.

Thiel’s former chief of staff, Michael Kratsios, directed the White House Office of Science and Technology Policy.

An executive from Anduril, a defense contractor backed by Thiel’s Founders Fund, was nominated as Army under-secretary while still holding up to $1 million in company stock.

This pipeline has paid off. In late 2024 and 2025, we saw a massive consolidation of federal power into private hands.

They have realized that the most profitable business model isn't just selling products to consumers. It is offering "governance as a service."

We look at this efficiency and applaud it. But it raises a difficult question: When a private company runs the software that powers the state, who is actually in charge?

Abundance for Them, Scarcity for You

This new system requires fuel. A lot of it.

The leaders of this shift love to talk about "abundance." Listen to Sam Altman or other AI evangelists, and they will tell you we are on the verge of a "fusion utopia." They promise that AI will eventually solve climate change and give us limitless, clean energy.

That is the sales pitch. And maybe, one day, it will be true. But the reality today is a story of immediate resource pressure.

To power the massive data centers required for their AI models, these companies are tapping into the American energy grid at an unprecedented scale.

According to the International Energy Agency (IEA), power consumption from data centers is projected to more than double... rising from 415 terawatt-hours in 2024 to 945 TWh by 2030.

To put that in perspective... that is roughly the equivalent of adding the entire electricity consumption of Japan to the global grid in just six years.

Where will this power come from?

Not from the magic fusion reactors of the future. It is coming from the grid you rely on today.

In the PJM electricity market, which covers 13 states from Illinois to New Jersey, the demand from data centers has already driven capacity prices up.

To meet this need, the government is pivoting. The Department of Energy is increasingly financing coal and natural gas expansion to keep the servers humming.

It creates a difficult dynamic:

It isn't necessarily malicious…It’s just math. But the math ends with the public paying higher bills to subsidize yet another part of the AI boom.

How "Efficiency" Is Deleting the Middle Class

This shift isn't just happening on your electric bill. It is happening in the workplace.

The stock market is rallying on the promise of "efficiency." And let's be honest, technology does make things more efficient. But for the workforce, "efficiency" often looks like a closing door.

We often look at headline-grabbing layoff numbers. And they are significant. In the first few months of 2025 alone, over 126,000 tech workers lost their jobs, according to Crunchbase.

But the bigger story is what happens after the layoff.

It is a phenomenon called "silent firing."

Companies aren't just letting people go. They are simply... not hiring replacements. When a worker leaves, the role is dissolved, or the tasks are handed over to software.

According to a report by Zety and Allwork, 73% of workers reported experiencing "quiet firing" tactics in 2025... where support is withdrawn and roles are made redundant without a formal announcement.

The entry-level jobs are being automated first. If you are a junior analyst, a copywriter, or a coder fresh out of college... the job you would have taken five years ago is harder to find.

This flattens the middle class. It creates a gap where new careers should be. And the industry leaders know this is happening.

The Trap of Outsourcing Global Sovereignty

This isn't just an American dynamic. This new model of "privatized sovereignty" is being exported globally.

Europe, for example, talks a lot about "Digital Sovereignty."

They want to be independent. But building your own tech stack is expensive and slow.

A report by the Centre for European Policy Analysis (CEPA) estimates that achieving true digital independence would cost Europe €3.6 trillion.

Most nations aren't willing…or able…to pay that bill. So, they sign contracts.

74% of publicly listed European companies now depend entirely on U.S. tech stacks.

Look at the United Kingdom.

The NHS signed a £330 million deal with Palantir to build its data platform. It’s efficient. It works. But it means a U.S. company now manages the health data of the British public.

Look at Ukraine. Their defense relies heavily on Starlink. It has saved countless lives. But it also means their military communications rely on the goodwill of a single American company.

It is a trade-off. These nations get the best technology in the world. But they become 'client states' in the process. You cannot have a truly independent foreign policy when your defense infrastructure is leased from a company in California.

And if a G7 nation can be reduced to a client state, the individual American worker doesn't stand a chance.

The architects know this. That is why they have prepared a specific 'safety net' for the people they intend to make obsolete.

UBI Is a Trojan Horse

We need to talk about the "safety net" the architects are promising us.

Every tech billionaire has the same talking point: AI is going to take all the jobs, so we will need Universal Basic Income (UBI).

It sounds generous. It sounds inevitable. But if you look at their actions, it looks less like a safety net and more like a trap. While they preach UBI in the future, they are actively dismantling the machinery required to fund it in the present.

Elon Musk frequently claims that UBI will be "necessary" in an AI future. Yet, he lead the Department of Government Efficiency (DOGE), an initiative explicitly designed to slash federal spending by trillions.

You cannot have it both ways.

You cannot gut the federal budget, fire the administrators, dismantle the tax collection agency (IRS), and then claim you are going to distribute a monthly check to 330 million Americans.

And it’s not like he’s going to give away his own money, either.

He recently stated: "The biggest challenge I find with my foundation is trying to give money away in a way that is truly beneficial to people."

He is literally telling us that he finds philanthropy "too difficult." If he can't figure out how to give away his own money, why should we trust him to build a system to give away the nation's money?

Sam Altman, the CEO of OpenAI, advocates for a "Moore's Law for Everything," where we tax capital to fund a citizen's dividend.

But his actual product, Worldcoin, reveals the true business model.

Worldcoin doesn't give you a dividend as a right of citizenship; it gives you a crypto token in exchange for scanning your iris. It creates a proprietary database of human biometrics owned by a private company.

This is a customer acquisition strategy. He wants to build a user base, not a social safety net.

And for figures like Peter Thiel, UBI isn't even meant to help the poor. They aim to delete the government.

UBI is the severance package for the "nanny state." The deal is simple: cut every citizen a check, and in exchange, eliminate Social Security, Medicare, and public infrastructure.

It sounds like freedom, but it is a bad trade.

Even if the check is large, it cannot replace the leverage of the state.

The government negotiates wholesale prices for healthcare and runs transit at a loss for the public good.

If you replace those systems with cash, you force individuals to buy "retail" in a market that knows exactly how much money they just received.

You are trading a durable right to services for a volatile subscription to them. And as any Netflix user knows, the price of the subscription always goes up.

Auditing the Myth of the "Self-Made" Empire

Before we talk about solutions, we have to look at the receipts. We need to audit the myth of the "self-made" techno-oligarch.

The narrative they sell is one of libertarian genius…that they built these empires in a garage, fighting against the heavy hand of the state.

The reality is that the state was their angel investor.

We…were their angel investor.

On top of the direct cash, the founders and CEOs have benefited from a tax code designed to let them hoard it.

The 2017 tax cuts slashed the corporate rate from 35% to 21%, and loopholes allow them to borrow against their stock holdings to live tax-free, while the average worker pays income tax on every paycheck.

Then there is the hidden subsidy: resource extraction.

When a data center drains a local aquifer to cool its servers, forcing the local town to upgrade its water treatment plant... the town pays for that upgrade. The company gets the cooling; the public pays the bill.

But it isn't just water. It is the air itself.

Despite the 'net-zero' press releases, the dirty secret of the AI boom is diesel.

To guarantee 99.999% reliability, these facilities rely on banks of massive generators.

In some counties, data centers are permitted to burn enough fuel to rival a major airport, pumping exhaust into local lungs to ensure a chatbot in California never lags.

And it is the noise.

These things are massive, concrete fortresses emitting a constant, low-frequency roar—a mechanical drone that penetrates walls and disrupts sleep for miles. It is the sound of local quality of life being liquidated for uptime.

Then there is the infrastructure bill.

The enormous power draw requires billions in new transmission lines. But the tech companies often aren't the ones paying for those upgrades…you are.

We have socialized the risks, the infrastructure costs, and the pollution, but privatized the profits, the intellectual property, and the control.

Demanding a Return on Our Investment

So... where do we go from here?

The old social contract was simple: Corporations make money, and in return, they provide jobs.

That contract is void.

They are building systems explicitly designed to remove the need for jobs.

The "Return on Investment" for the public is no longer employment. And it certainly isn't UBI, which remains a distant fantasy while the tax base to pay for it is eroded.

If the public is going to put up the capital, and deal with the consequences of ballooning energy and resource use, the public should see a return.

We need a new model for ROI.

The Sovereign Equity Model

In the venture capital world, if an investor puts up the money to de-risk a technology, they get equity. They get a seat on the board. They get a share of the upside.

Yet, when the U.S. taxpayer does it, we call it a "subsidy."

The CHIPS Act alone funneled $52 billion into semiconductor manufacturing…

While the taxpayers who funded this got nothing but the bill.

This is bad business.

We need to adopt a Sovereign Equity Model.

If a company wants a government loan, a tax credit, or a guaranteed energy contract, the government should take equity warrants in return. This isn't radical socialism… It’s basic capitalism.

It is exactly what Warren Buffett did when he bailed out the banks in 2008. He didn't give them free money…he bought warrants that eventually made Berkshire Hathaway billions.

We already have a successful blueprint for this in the Alaska Permanent Fund.

Since 1976, the state of Alaska has treated its oil reserves not as private bounty, but as a shared asset. When the oil flows, a portion of the revenue is deposited into a sovereign wealth fund, which then pays out an annual dividend to every resident.

We should treat our digital and energy infrastructure the same way.

The profits from these government-backed equity stakes shouldn't disappear into the black hole of the general budget; they should flow into a ring-fenced National Wealth Fund that pays dividends directly to the citizenry.

If the American people are taking the risk, we should own the upside.

Tax the Robots to Save the Tax Base

The U.S. tax code is currently rigged to favor machines over people.

If you hire a human, you pay payroll taxes, social security, and healthcare. If you buy a GPU cluster to do the same job, you get a tax write-off for "depreciation." We are effectively subsidizing our own replacement.

We need to rebalance the ledger with an automation adjustment.

This is not about punishing innovation… It’s about fiscal survival. Payroll taxes consistently account for roughly 30-35% of all federal revenue. If AI fulfills the promise of displacing millions of workers... that revenue stream collapses. The deficit explodes. The economy breaks.

Bill Gates, hardly a socialist, made this point explicitly: "Right now, the human worker who does $50,000 worth of work in a factory... that income is taxed... If a robot comes in to do the same thing, you’d think that we’d tax the robot at a similar level."

If a company replaces a human workflow with an AI agent, the economic output remains, but the tax contribution vanishes. We need to attach a levy to that output.

Data Dividends

Data is the new oil. We have heard the cliché a thousand times. But we aren't treating it like oil.

The AI models generating trillions in value were trained on the collective output of humanity. They scraped our journalism, our art, our open-source code, and our personal data. They harvested the "digital commons" for free... processed it... and are now selling it back to us at $20 a month.

In any other industry, this would be theft. If you drill for oil on someone else's land, you pay royalties. If you use someone else's timber, you pay for the lumber.

The generative AI market is projected to reach $1.3 trillion by 2032….

The raw material that fuels that market cannot be priced at zero. If our data is the raw material for their product, we are the suppliers. And suppliers get paid.

Universal Basic Services

If we give everyone a $5,000 UBI check, but the price of housing, energy, and internet doubles... we haven't solved anything. We have just subsidized the landlords and the utility companies.

The smartest Return on Investment is to lower the "overhead" of being alive in America.

We should move toward Universal Basic Services (UBS). Use the proceeds from the equity stakes, the automation taxes, and the data dividends to fund the inputs of the modern economy:

We are hitting the physical limits of our energy grid. We are seeing the limits of the old labor model. We might have to accept that "infinite growth" isn't compatible with a finite planet.

But "no growth" doesn't have to mean poverty.

The vibes are off because deep down... we know the deal has changed. We are moving from a world of public institutions to a world of private platforms.

The "New Operating System" is being installed. And it is faster. It is more efficient. It is undeniably impressive.

But we have to decide if we want to be the owners of this new future... or just the users.

https://oilprice.com/Energy/Energy-General/Why-Does-the-End-of-the-World-Look-So-Profitable.html

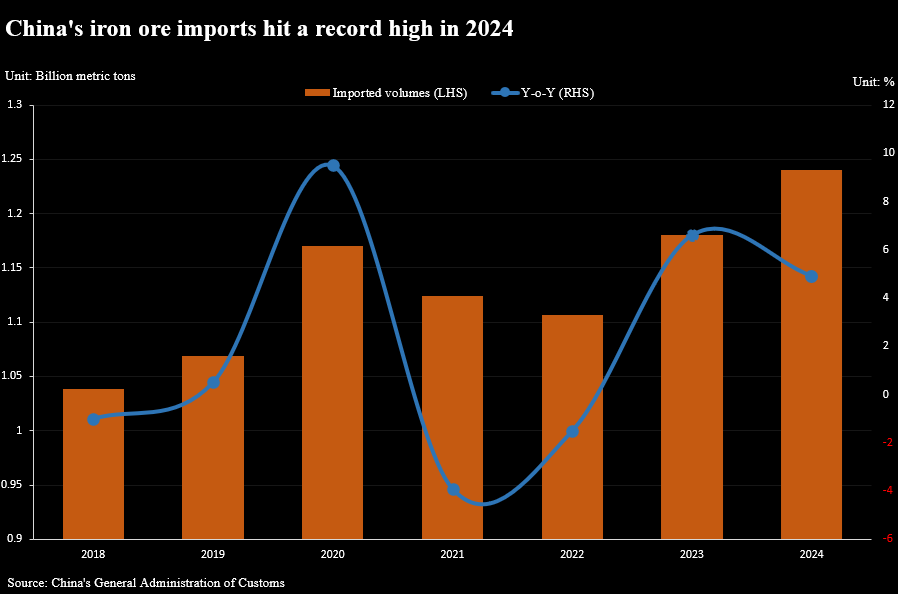

Crude oil and iron ore stocks climbed in November, while copper and coal imports slipped, with stable prices guiding the diverging trends.

Finimize Newsroom

4 hours ago

What’s going on here?

China's latest import numbers paint a split screen: crude oil and iron ore shipments surged in November, while appetite for copper and coal faded. It's not demand driving the change – it's steady prices setting the tone for the world's top buyer.

What does this mean?

In November, China ramped up crude oil imports to 12.38 million barrels a day – the highest in over two years – as stable Brent prices gave refiners the green light to stock up. Iron ore deliveries held strong at 110.54 million tons, with stockpiles climbing to their highest point since February, thanks to pricing stability on markets like Singapore. Copper tells a different story: refined imports slipped to 427,000 tons, squeezed by higher global prices and a rush from US buyers ahead of expected tariffs. Coal’s trend is mixed – November’s arrivals edged up from October, but sat nearly 20% below last year, and the 2025 cumulative tally is down 12%. In short, China's latest moves suggest the steadiness or shakiness of prices is steering trade flows more than old-fashioned demand levels.

Why should I care?

For markets: Price cues take center stage for global traders.

China’s commodity moves can shake up global markets from Singapore to Wall Street. The confidence steady oil and iron ore prices give to buyers and sellers props up contract stability across the board. But with copper and coal trending lower on price pressure rather than demand, savvy traders may start focusing on price signals over raw consumption when weighing up future moves.

The bigger picture: Global supply deals get a pricing reality check.

China's import patterns signal a global reset, with pricing trends now guiding the raw materials trade. Exporters and policymakers everywhere may need to rethink how they measure risk, plan supply deals, and manage inflation pressures. As the world’s biggest buyer leans into price as the top driver, old-school supply and demand forecasting just got a lot more complicated.

https://finimize.com/content/chinas-commodity-imports-split-as-price-trumps-demand

By RFE/RL staff - Dec 08, 2025, 9:00 AM CST

Ukrainian President Volodymyr Zelenskyy was set to meet with key European allies after US President Donald Trump accused him of not reading the latest peace proposal.

The December 8 talks in London follow three days of negotiations between Ukrainian and US officials near Miami as negotiators try to find agreement following the release of a US draft peace proposal last month.

The 28-point plan was seen as heavily favorable to Russia, and Kyiv has pushed back on some of the more strident, hard-line demands that President Vladimir Putin has pushed since before he launched the full-scale invasion of Ukraine in February 2022.

"We are starting a new diplomatic week right now -- there will be consultations with European leaders. First and foremost, security issues, support for our resilience, and support packages for our defense," Zelenskyy said in his nightly address, recorded on a train on December 7.

Zelenskyy's London meetings include Kyiv's biggest backers in Europe: British Prime Minister Keir Starmer, French President Emmanuel Macron, and German Chancellor Friedrich Merz.

Meanwhile, in Washington on December 7, US President Donald Trump criticized his Ukrainian counterpart, saying he was "a little bit disappointed."

"We've been speaking to President Putin and we've been speaking to Ukrainian leaders, including Zelenskyy, President Zelenskyy, and I have to say that I'm a little bit disappointed that President Zelenskyy hasn't yet read the proposal, that was as of a few hours ago," Trump told reporters.

Ukraine's chief negotiator, Rustem Umerov, said he would report to Zelenskyy on the latest developments on December 8.

One of Kyiv's main goals in the Miami talks was to obtain "all drafts of current proposals in order to discuss them in detail with the President of Ukraine," Umerov wrote on X. "Today, we will provide the President of Ukraine with full information on all aspects of the dialogue with the American side and all documents."

Details of the proposal following adjustments to the 28-point plan have not been released publicly, and Trump said nothing about its content. US and Ukrainian officials have indicated in recent days that key sticking points included control over territory and security guarantees for Ukraine.

Ukrainian political analyst Volodymyr Fesenko said that while "we don't know don't know exactly what the United States is proposing," a clause from the 28-point plan obliging Ukraine to withdraw its forces from territory it still controls in the Donetsk region could be a major barrier to any agreement.

"The majority of Ukrainians, despite all current difficulties, are unlikely to accept the idea that Ukraine voluntarily leaves the Donbas without receiving anything in return, not even real guarantees of a cease-fire," Fesenko, head of the Penta Center for Political Studies in Kyiv, told Current Time.

In uncompromising comments last week, Putin said Russia would seize control of the Donbas -- the Donetsk and Luhansk regions -- "by military or other means," suggesting Moscow would not agree to a deal that leaves any part of the region in Ukrainian hands.

He said the same of the part of Ukraine once known in Russia as "Novorossia," indicating Moscow might also demand full control over the Zaporizhzhya and Kherson regions. Ukraine still holds large parts of the two southern regions, including their capitals.

Following the negotiations in Miami, Zelenskyy said he had spoken with US special envoy Steve Witkoff and Trump's son-in-law Jared Kushner, who have led the negotiations on behalf of the White House.

"The American envoys are aware of Ukraine's core positions, and the conversation was constructive though not easy," Zelenskyy said.

Meanwhile, Russia continued its air strikes on Ukrainian infrastructure as winter temperatures fall.

Russian forces attacked Okhtyrka in the Sumy region on the night of December 8, according to regional authorities.

Governor Oleh Hryhorov said seven people were injured in a strike on a nine-story residential building, all of whom were taken to a hospital.

According to Ukrainian emergency officials, firefighters extinguished a blaze on the second to fifth floors and evacuated 35 residents, rescuing seven people, including one child, from damaged apartments.

In Chernihiv, an apartment building was damaged as a result of the fall of a Russian drone. Three people were injured, one of whom was hospitalized, emergency officials said in a post to Telegram.

Ahead of Zelenskyy's planned visits to Brussels and Rome this week to discuss the peace process, the Ukrainian leader spoke by phone with Italian Prime Minister Giorgia Meloni.

Meloni reaffirmed Rome's solidarity with Kyiv and pledged to supply emergency aid to support Ukraine's energy infrastructure and its population, according to a statement from her office.

The office added that Italy will deliver additional supplies, including generators, to support energy infrastructure and the Ukrainian population, and that the goal remains a lasting and just peace.

New York — Just a few weeks ago, the stock market stumbled over fears that artificial intelligence stocks might be in a bubble. Now stocks are back within reach of a record high.

Thank the Federal Reserve.

The market has rebounded from a dip in early November as investors have leaned into bets that the Fed will cut interest rates this week at its last policy meeting of the year.

Interest-rate cuts can boost stocks by lowering savings rates and borrowing costs for individuals and businesses, in turn encouraging spending and investing, spurring business activity and increasing corporate earnings.

Fed rate cuts can also lower the yield on short-term government bonds and cash equivalents like money market funds, making higher-yielding assets like stocks more attractive to investors.

All told, interest-rate cuts can create a strong tailwind for stocks.

Holiday decorations outside the New York Stock Exchange (NYSE) in New York on December 8, 2025. Michael Nagle/Bloomberg/Getty Images

Jonathan Krinsky, chief market technician at BTIG, said in a Monday note that the stock market’s recent rise has coincided with increasing odds for a Fed rate cut in December.

Traders on Monday were pricing in an 89% chance the Fed cuts rates, according to CME FedWatch.

“Markets have essentially seen a complete reversal of November’s weakness,” Krinsky said. “This has coincided almost in lock-step with rate-cut odds for the upcoming December (Fed) meeting.”

Lower rates can boost stocks

The Fed is cutting rates in response to concerns about a weakening labor market. But for investors, lower rates can provide fuel for stocks to rally.

The Fed’s benchmark interest rate influences a range of interest rates across the economy. A Fed rate cut can lead to lower financing costs for a broad range of companies.

The Russell 2000, a market index of smaller companies that are more rate-sensitive, hit a record high on December 4.

“When you look at the firms that are more vulnerable and are smaller, like those in the Russell 2000, when you have lower rates, their interest expenses drop heavily, and that widens their profit margins,” said José Torres, senior economist at Interactive Brokers. “That’s really why areas like real estate, manufacturing and small businesses benefit a lot more from lower rates.”

To be sure, while investors have embraced hopes for a rate cut this week, Wall Street is always forward-looking, and there is less certainty about the path of rate cuts in January.

The Fed on Wednesday will release its quarterly summary of economic projections, which lays out — anonymously — officials’ expectations for the course of interest rates across the coming months.

“As the (Fed) considers additional rate cuts at its meeting this week and into 2026, reaccelerating inflation would likely force a slower, more cautious path,” Jayson Pride, chief of investment strategy and research at Glenmede, said in a note.

https://www.cnn.com/2025/12/09/business/us-stock-market-federal-reserve-rate-decision

By Li Jing

Nation seeking to strengthen long-term innovation capacity, modernization

China is expected to step up the efficiency of its proactive fiscal policy next year, sharpening its focus on expanding domestic demand and strengthening long-term innovation capacity — priorities experts say will anchor China's economic strategy for the 15th Five-Year Plan (2026-30).

In a recent signed article published in People's Daily, Finance Minister Lan Fo'an said fiscal authorities will "comprehensively expand domestic demand" and "support high-level technological self-reliance and self-strengthening", adding that active fiscal policy must be carried out "with greater strength and higher efficiency" to underpin the next stage of Chinese modernization.

Analysts said Lan's piece offers one of the clearest signals of the priorities likely to be set during the upcoming annual Central Economic Work Conference.

Lan wrote that fiscal measures will play a central role in unlocking consumption potential and increasing household income through tax, social security and transfer-payment measures, while cultivating new areas of consumer demand. He called for broader use of fiscal subsidies and interest-rate incentives to build new consumption scenarios, alongside special-purpose bonds and ultra-long term special treasury bonds for long-term structural investment.

The minister underscored that public finance must remain "people-centered" and that more resources should be invested "in people and for people" by combining physical and social infrastructure to sustain long-term demand.

This shift represents "a profound adjustment", said Qiao Baoyun, a professor at the China Academy of Public Finance and Policy at the Central University of Finance and Economics. "The article highlights a greater tilt of fiscal resources toward people and social welfare. It stresses that people are the goal and materials are the means."

Experts expect the upcoming conference to outline more concrete steps to stabilize consumption and investment. Tian Lihui, university chair professor of finance at Nankai University, said domestic demand expansion and technological self-reliance will form "two wings of the same logic chain", supported by a more proactive fiscal stance and moderately accommodative monetary policy.

"The policy approach combines 'more active fiscal policy' with 'moderately accommodative monetary policy', while introducing a consistency assessment across macro policies, bringing economic and noneconomic policies into a unified framework to enhance the foresight, precision and effectiveness of countercyclical measures. It forms a policy 'combo punch' that helps hedge against external uncertainties and strengthens institutional support for improving total factor productivity," Tian said.

He added that coordinated measures, from income boosting for middle- and low-income groups to diversified consumption scenarios and equipment-upgrade initiatives, will help generate tangible progress and attract more private capital.

Lan also called for stronger fiscal support for basic and applied research, national strategic science and technology tasks, and breakthroughs in key core technologies. Tools such as tax incentives, government procurement and investment funds will help upgrade traditional industries, nurture emerging and future industries, and promote deeper integration of technological and industrial innovation.

Tian said the innovation push will evolve toward ecosystem building, with mechanisms such as "open competition for selecting leading teams" and "horse racing "parallel competition initiatives playing a larger role in frontier fields including artificial intelligence and biomedicine.

One example is the recent financing by METiS TechBio, an AI-driven nanodelivery company, which secured funds from Beijing-based healthcare investment institutions to support platform building and technology translation, illustrating how fiscal and industrial policies jointly strengthen innovation capacity.

International observers also expect China to maintain a supportive fiscal environment while managing risks. Alex Muscatelli, director of sovereign economics at Fitch Ratings, said China's fiscal stimulus was ramped up in the first half, not only through consumer-support measures such as trade-in programs, but also through infrastructure spending.

Russian foreign minister Sergei Lavrov is speaking at the Federation Council this morning.

According to state news agency TASS, he praised Donald Trump for being the "only Western leader" showing an understanding of Moscow's position on Ukraine.

Lavrov also took aim at the UK and EU, saying both were in "hopeless political blindness" and were deluding themselves with the illusion of overcoming Russia.

TASS further reported Lavrov said Moscow has no intention of going to war with Europe.

Instead, Russia remains ready to respond if troops are deployed in Ukraine.

Lavrov spoke on his peace plan discussions with US envoy Steve Witkoff in Moscow last week, saying Trump's top negotiator talked about the need to ensure the rights of national minorities in Ukraine.

Featured

Thanksgiving Thoughts - and The Year Ahead for Commodity Investors

Commodity Intelligence Comment - Thu 08:52, Nov 27 2025

The Commodity Intelligence/Burdass View - We Filtered the Noise in 2025 - Looking Ahead to 2026

If 2024 was the year of Waiting for the Pivot, 2025 has been the year of Divergence. The rising tide is no longer lifting all boats. We have been in a market where commodity correlations are breaking down—most notably the historic decoupling of gold (bullish) and oil (bearish/complex). Commodity Intelligence has been on the right side of these shifts and we hope that you, our clients, have profited.

If 2025 was about Divergence, 2026 is to be the Year of Consequence.

For five years, the market has traded on "paper promises"—promises of seamless green transitions, promises of endless shale supply, and promises that inflation was transitory. In 2026, those narratives start to hit the wall of physical reality.

The "noise" in the coming year will be about weak growth and demand destruction (recession fears). Our "signal" is the Supply Cliff. We are entering a window where capital starvation in parts of the mining sector is finally showing up in the physical delivery numbers.

Focus Commodities for 2026

Gold

2024 was the Stealth Bull Market. We saw it developing at Commodity Intelligence, yet we are not sure if the generalist investor was on top of it.

2025 brought the rise of the Eastern Central Bank Buyer. We believe China bought a lot more gold than it disclosed and is becoming the non-aligned world's gold custodian. U.S. Treasuries no longer seemed as attractive as they did historically to these buyers.

What about 2026? We think this could be the year when the Western institutional Buyer capitulates and joins the gold party. The driver is fiscal dominance. With Western debt interest payments becoming unmanageable, the market is realising that "real rates" don't matter if the currency itself is being debased to pay the bills.

What should you be doing in your gold portfolio? We think that the royalty companies are now starting to look expensive. There's relative value in Anglogold. Of the majors, Barrick looks more interesting than Newmont at the moment. With Elliott Management inside the tent and the Old Guard exiting, Barrick is no longer a 'value trap'—it is an event-driven breakup play. We are buyers of this volatility. Small caps like resource-heavy Seabridge are front of mind from a fundamental valuation perspective. This is our preferred smaller play, yet there will be other small and mid-caps that have cleaned up their balance sheets and are now better candidates for M&A activity.

Copper

In H1 2025, our view was that copper was heading for a near term surplus. This was reasonable based on the data we had at the time and the views of the International Copper Study Group (ICSG).

The outlook has changed, based not on accelerated energy transition or stronger growth, but a string of major outages, most notably at Grasberg in Indonesia.

We now see copper heading for a modest deficit of 250,000-300,000 tonnes (1-1.25% of the market). The risk to that forecast could be toward a greater deficit if further mine level incidents occur.

The market is obsessed with the mine hole at Grasberg, but it is missing the smelter crisis. Chinese scrap availability has collapsed. The supply chain is short from both ends.

We see First Quantum as a strong play on copper with pure alpha should Cobre Panama return to the portfolio. Even should this not happen, a $5.50/lb copper price should act as a tailwind.

Uranium

We have been closely tracking the return of demand for nuclear power stations, especially in the U.S. and UK but also elsewhere.

The Inventory Overhang narrative is dead. We are now seeing a scramble for physical pounds.

The easy beta trade (physical trusts) is over. The alpha in 2026 belongs to the Permitted Western developers—the only ounces that can legally satisfy the new data-center baseload contracts.

Oil & Gas

We see the potential end of the Ukraine war coming into the near-to-mid-term investment horizon. The Commodity Intelligence view on oil prices for this cycle sees a bottoming process in the $50s, with a hard floor at $45 driven by U.S. shale breakevens. We aggressively refute the 'oil to $30' bear case.

From an equity perspective, the sector is providing relatively strong dividends and has taken bold measures to cut costs, especially its corporate HQ footprint, during 2025.

At a stock level, our focus on BP over Exxon continues. Special situations get more interesting where there is no directional price momentum to move the stocks. We carried a story recently suggesting one of the last major oil bulls has given up the call; our view is that the market may become less sensitive to the last few dollars of oil price downside from an equity perspective.

The year ahead will be volatile, but for the disciplined investor, volatility is just the entry fee for value. Stay with the signal, ignore the noise.

Featured Commodity Intelligence Comment - May 20th 2025

China Now Forming More Households than Homes?

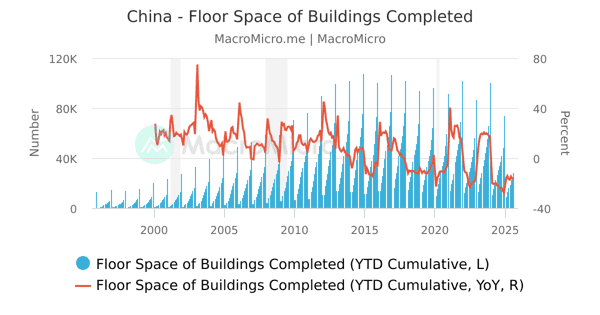

"Moreover, property investment in China fell 10.3% in the first four months of 2025 from a year earlier"

China’s property sector continues its structural unwind. Investment fell 10.3% year-on-year in the first four months of 2025, but the more telling figure is the 23.8% collapse in new floor space starts—a clear signal of developer retrenchment. Sales are also falling, down 2.8%, confirming ongoing demand-side weakness.

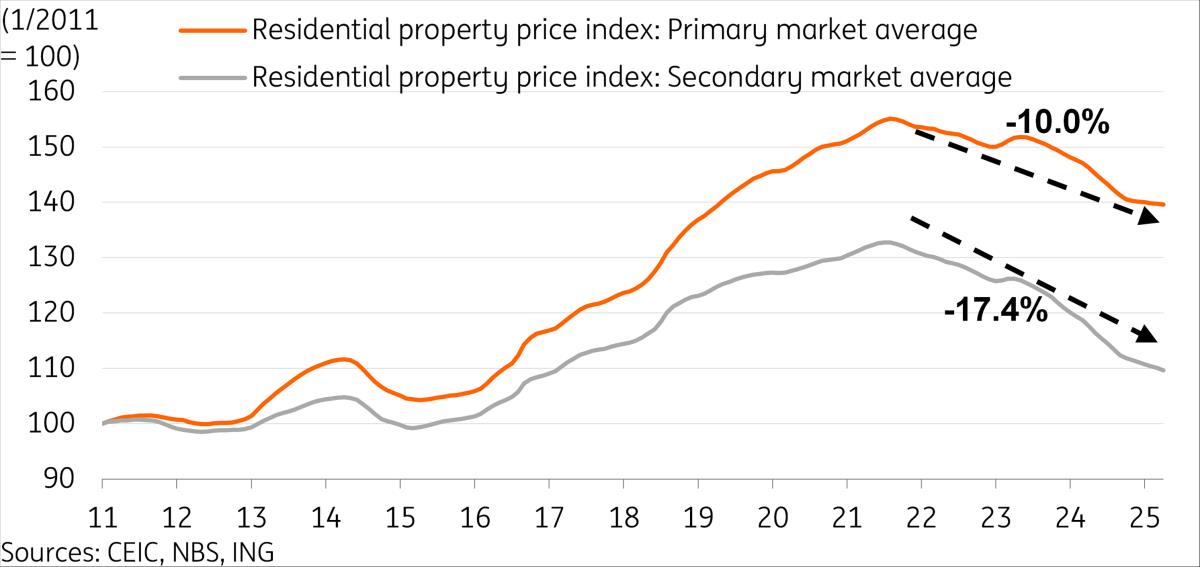

More striking still is the price picture. Used home values are now just 10% above 2011 levels, meaning Chinese real estate has posted negative real returns for over a decade. In a country where property once anchored middle-class wealth, this is a profound shift.

Overbuilding in lower-tier cities looks indisputable, with construction in some areas having run 3–5 years ahead of actual household formation. Data discrepancies between population registers and household records further cloud demand forecasts. Commodity Intelligence openly questions the integrity of China’s demographic data, with discrepancies emerging between population counts, police data and household registrations—raising further questions about the underlying demand assumptions that underpinned the boom.

While local governments are now buying excess inventory and easing credit conditions, the road to recovery looks long. In Zhengzhou, part of a five-city group reducing inventories, unsold stock fell by over 1.3 million m²—progress, but against a still-high national backdrop.

New housing starts in 2024 were just 739 million m²—only ~33% of the 2019 peak—and likely lower in 2025. With long-run sustainable demand estimated at ~800 million m², supply has now dipped below equilibrium, but inventories remain bloated.

In our view, this is not a V-shaped rebound. It’s a long reset. And for commodity investors, the message is stark: China is now forming more households than it is building homes for—proof that the property bubble has well and truly burst.

These are dynamics we’ve tracked closely at Commodity Intelligence, supported by on-the-ground insight from Beijing to Anhui. For clients seeking deeper data or regional analysis, we’re happy to provide more.

Original story from the news below:

SINGAPORE: Iron ore futures prices fell on Monday, pressured by tepid economic data from top consumer China and uncertain near-term demand for the steelmaking material.

The most-traded September iron ore contract on China’s Dalian Commodity Exchange traded 1.03% lower at 721.5 yuan ($100) a metric ton, as of 0258 GMT.

The benchmark June iron ore on the Singapore Exchange was 0.56% lower at $99.5 a ton.

Broadly, growth in China’s industrial output and retail sales slowed in April, official data showed on Monday, as a trade war threatened to dampen momentum.

Moreover, property investment in China fell 10.3% in the first four months of 2025 from a year earlier, following a drop of 9.9% in the first quarter, official data showed on Monday.

Hot metal output, typically used to gauge iron ore demand, fell 8,700 tons month-on-month to 2.45 million tons, said broker Everbright Futures, which attributed the fall to blast furnaces undergoing maintenance.

Total iron ore stockpiles across ports in China also grew, inching up 0.26% on-week to 137 million tons as of May 16, Steelhome data showed.

Still, production among Chinese electric-arc-furnace steel producers ended its two-week slide and increased again on May 15, as hopes for better profits and higher steel demand encouraged the mills to lift output, said consultancy Mysteel.

“The number of profitable blast-furnace steel mills in China continued to increase this week, mainly thanks to the recovery in finished steel prices,” added Mysteel in a separate note.

Other steelmaking ingredients on the DCE languished, with coking coal and coke down 2.43% and 2.17%, respectively.

Steel benchmarks on the Shanghai Futures Exchange lost ground.

Rebar fell 1.03%, hot-rolled coil weakened 1.11%, wire rod fell nearly 1.5% and stainless steel eased 0.19%.

Featured

The End of The Global Carry Trade

Japan’s 10-year government bond yield climbed above 1.77% on Wednesday, marking a fresh 17-year high ahead of a crucial debt auction that could indicate investor demand amid rising fiscal concerns.

The Ministry of Finance plans to auction around 800 billion yen in 20-year JGBs.

On Tuesday, the government proposed a supplementary budget exceeding 25 trillion yen to fund Prime Minister Sanae Takaichi’s stimulus plan, far above last year’s 13.9 trillion yen extra budget, stoking debt worries.

Meanwhile, Bank of Japan Governor Kazuo Ueda told the prime minister that the central bank is gradually raising rates to steer inflation toward its 2% target while supporting sustainable growth.

Afterward, Ueda told reporters the prime minister made no specific request on monetary policy.

On the data front, machinery orders in Japan rose more than expected in September, signaling robust capital spending.

https://tradingeconomics.com/japan/government-bond-yield

Commodity Intelligence Comment - Wed 07:49, Nov 19 2025

Feature by James Burdass:

The Japan Connection:

For much of my investment career, investors have engaged in the well known "carry trade". I had a front row seat at Mitsubishi UFJ Trust during the late 2000's, working for a Japanese institution. During that time, I advised on the major GPIF account, one of the largest single mandates in the world.

I led on Materials in the World ex-Japan. Japan has a unique role as the world's largest creditor nation. As readers know, it has historically been the largest single holder of US treasuries (holding over $1.1 trillion).

Japan's persistent current account surpluses averaged approximately $127 billion annually from 2020-2023 according to the Ministry of Finance Japan. These surpluses have allowed Japanese institutions to accumulate massive foreign asset holdings over decades.

Look at the chart in the link above. It's obvious that the interest rate environment in Japan is changing and the risks of such a structural shift are significant, yet we flag a risk that the market is too complacent about it.

What's the problem here?

For many years, investors have borrowed funds at virtually 0% from Japan and then converted to US Dollars or to Euros to buy higher yielding assets (like US bonds or stocks).

Asian buyers (and others using the carry trade) therefore become key funders of the US fiscal deficit and stock markets.

Now Japan, having raised rates earlier in the year, looks to increase them further. The issue with Japan raising rates is that, with the yield on the 10 year JGB at 1.77%, the market is perilously close to assigning something resembling a normal interest rate to Japan again, for the first time in many investor's memory.

A New World Order, with fracturing trade routes and trading blocs has already dampened non-aligned Government and investor appetite to fund the US deficit. After all, if free trade is blocked, why is Beijing obliged to fund it?

As Japan raises rates, this cheap borrowing disappears. Investors will be concerned that others may be forced to unwind these trades, which then involves selling the foreign assets and buying back the Japanese Yen.

In 2024, as this trend first began, there were some shockwaves, initially in Asian markets such as the KOSPI. However, since that time, investors seem to have become largely complacent about this risk. This is despite the clear shift that a non-zero interest rate would give to an institutional investor like Mitsubishi. The incentive becomes to repatriate capital to Japan. This effect can potentially have second order effects - upward pressure on borrowing costs in other countries, too.

This is the most visible threat to global liquidity that we have seen for some time.

The Good News

There is a little bit of good news here. Rate hikes from the BoJ mean that Japan feels it may have beaten its multi-decade long fight against deflation. Inflation has been persistent (above 2% for several years now) and wage growth continues.

Next steps

The Takaichi administration is clear in its position that the BoJ should not raise rates further at the December meeting (a rise from 0.5% to 0.75% is thought possible). This is a meeting that will have important effects, not just for Japan but also for global liquidity.

Conclusion

The structural risk of the Carry Trade unwinding requires investors to seek protective positions and identify beneficiaries of capital repatriation.

Commodity Impact

The Bank of Japan is closing the door on two decades of global monetary subsidy. While political noise will continue through the December meeting, the fundamental shift toward JGB normalisation means the cost of funding the US deficit is set to rise, and there's a risk that global liquidity could contract.

The clearest commodity beneficiary from this is gold. If investors become less complacent about US fiscal risk, this would encourage central banks to continue topping up their gold positions. Should the US Federal Reserve be seen to be managing debt interest costs, again this comes back to a preference for the yellow metal.

In summary, the rise in Japanese interest rates acts as a systemic stressor on the global financial system. Since gold is a non-debt, anti-systemic asset, the increase in volatility, uncertainty, and sovereign debt risk makes the metal a prime beneficiary. Commodity Intelligence scored a major win for clients by calling gold higher in 2025, we have recently said that gold can progress to $4,750 during 2026.

For areas other than precious metals, this is a risk - we think more people should be talking about it in a wider market that seems fully focussed on disruptors and potentially overvalued AI plays in a market saturated with technology bulls. We would be interested to hear your views, too, at james@commodityintelligence.com.

Featured

Beyond the Barcelona Sun: Divergent Paths for BHP and Rio Tinto

Codelco announced on its website that at the Bank of America Merrill Lynch Global Metals, Mining & Steel Conference, BHP and Codelco unveiled an exploration agreement targeting the state-owned company's assets in the Antofagasta region.

The agreement is subject to the requirements stipulated in Law No. 19,137, which outlines the conditions for Codelco to collaborate with third parties in developing mining projects that are not currently operational or are not part of the company's decision to allocate them to its replacement or expansion plans through direct development.

In 2022, Codelco offered 34 exploration assets to interested companies to assess the possibility of collaborative development for projects that do not meet the criteria for independent development by the company.

This portfolio includes the "Anillo" mining area, located in the Antofagasta region and spanning 24,000 hectares. The mine is currently in the early exploration stage, with Codelco and third parties having conducted multiple exploration activities there in the past.

"The company must focus on and prioritize its exploration and investment efforts within the approximately 2.3 million hectares of mineral resources it holds in Chile. We possess some highly promising mining concessions, and to expedite their development, we must advance collaborative approaches aimed at capturing value through partnerships with third parties. Our collaboration with BHP, one of the world's largest mining companies, is an example of this," explained Maximo Pacheco, Chairman of Codelco's Board of Directors.

BHP has unique advantages in exploring this project, and if successful, it will possess unique infrastructure capabilities to accelerate the project's development. As part of the agreement, the polymetallic mining company will be able to invest up to $40 million to explore and study the mining potential of the ore deposit.

Mike Henry, CEO of BHP, stated, "BHP is one of the world's leading copper producers, and copper is a crucial metal driving economic development, decarbonization, and digitalization. We are delighted to explore this collaborative opportunity with Codelco, with whom we already have a significant and successful mining presence in Chile. Our ongoing commitment to innovation and our 140 years of experience in mining project development enable us to partner with Codelco to deliver more copper to the world."

If a sustainable business case is established, the contract will include a commitment to collaborate with Codelco in developing the project. If the application is unsuccessful, the research and information obtained will become the property of Codelco.

Commodity Intelligence Comment - Wed 08:53, May 14 2025

Here is our take on Mike Henry's speech at BAML's conference in Barcelona and how the messaging contrasts with Rio Tinto's remarks:

Mike Henry’s 2025 address marks a clear evolution in BHP’s strategic messaging. What stands out is Henry’s emphasis on BHP’s role as a “point of stability” in an increasingly uncertain global environment. This rhetorical pivot showed BHP’s intent to not just weather instability but actively position itself as a safe harbour investment. While operational excellence and capital discipline remain core themes, the speech more forcefully links these traits to BHP’s ability to navigate extremes—from intensified trade wars to potential economic fragmentation.

We thought that a particularly noteworthy update was the growing prominence of copper and potash in BHP’s portfolio. Henry announced that copper now represents 39% of BHP’s EBITDA, and confirmed that production has grown 24% since FY22—a substantial shift that reaffirms copper’s role as a long-term strategic pillar. Furthermore, the Vicuña Joint Venture (previously lesser known) was presented as a transformational copper development, with its integrated potential positioning it among the top ten global copper producers. This was complemented by a first-time disclosure of 38 million tonnes of copper resources within the JV and confirmation of a forthcoming technical report in Q1 2026—clear signals of BHP’s accelerating copper ambitions.

Potash has clearly emerged as a central theme, showing BHP’s deeper commitment to agricultural minerals. While Jansen has been discussed in past forums, Henry’s 2025 speech was much more confident and assertive in comparing it structurally to iron ore—highlighting low-cost potential, jurisdictional stability, and scalability. BHP securing MOUs with global buyers is new and material, reinforcing confidence in commercial viability as Jansen ramps up.

Finally, Henry’s remarks reflected a more assertive tone on productivity gains via the BHP Operating System (BOS). New data points—like Western Australia Iron Ore (WAIO's) ~$8 per tonne margin advantage over competitors—were used to emphasize BOS’s impact. Extending this system to Escondida could bring a second wave of performance improvement, over and above operational maintenance.

We noted with interest BHP's view that iron ore enjoys cost support at $80 per tonne. Our sense is that this floor could be lower than BHP thinks, especially as steel capacity comes out of China and Simandou hits the market.

By comparison to BHP's talk of stability, Rio Tinto was more focussed on growth. The company is now targeting a return to CAGR at 3% 2024-2033 and is highlighting growth from Oyu Tolgoi, Simandou, Rincon, Nuevo Cobre, Resolution and Arcadium.

This is potentially a differentiator between the two companies. We think that BHP is positioning itself as the strongest company in the industry in an uncertain world, whereas Rio sees itself attracted to fresh growth opportunities. As we have previously mentioned in the Daily, this is the result of decisions that were set in motion some time ago. Rio Tinto's strategic pivot towards battery materials is also evident in their acquisition of Rincon and the recent Arcadium Lithium merger, positioning them to capitalise on the energy transition. This focus on growth, particularly in copper and lithium, suggests a higher risk appetite compared to BHP's more conservative stance.

Not everyone at BHP is happy with the relative lack of growth. Indeed, they attempted to buy Anglo American for more copper exposure. We still see a possibility that the internal bureaucracy pivots back to M&A, yet a key takeaway is that it was absent from the speech. The new "Anillo" mine exploration adds an interesting early phase exploration opportunity.

We have run through in our recent feature the candidates for the new CEO. Perhaps the unspoken message is not that change is off the table, but that it may be paused until a new CEO is in place.

The transcript is here:

Our balance sheet shows that the surplus in the oil market is set to grow in 2026, following OPEC+'s decision to unwind supply cuts at a quicker-than-expected pace. Non-OPEC supply is also expected to grow at a healthy clip despite this year's price weakness.

According to our balance, we will see a surplus of more than 2m b/d in 2026. Global supply is set to grow by 2.1m b/d next year, while demand looks to be more modest at around 800k b/d.

The peak of this surplus is expected in the first half of 2026. However, with our balance sheet showing a surplus in every quarter next year, global oil stocks should continue to build through the year, keeping downward pressure on prices. We forecast that ICE Brent will average US$57/bbl over the year, with the key assumption being that Russian oil flows continue unabated despite US sanctions on Rosneft and Lukoil.

The scale of the surplus and the expected build in inventory should put the forward curve under additional pressure, pushing it deeper into contango. The front end of the curve has held up better than expected as supply risks provide support. In addition, the growing amount of Russian oil at sea not making its way to the destination suggests the spot market may be tighter than what the oil balance suggests at the moment.

This is a key risk to our bearish view. Clearly, if sanctions prove more effective than we and the market expect, this leaves upside for oil prices. However, Russia has managed to keep oil flowing since 2022 despite sanctions and embargoes. We suspect the use of intermediaries and the larger discounts available to buyers of Russian crude oil should see flows continue.

Downside risks include ongoing peace talks. If they lead to the lifting of certain sanctions on Russia, much of the supply risk hanging over the oil market will ease. While we don’t believe such a scenario would dramatically increase Russian oil supply, given that it’s held up well despite sanctions, removing this risk could push Brent down to the low $50s.

https://think.ing.com/articles/bearish-oil-outlook-but-clear-upside-risks/

SOFIA, Bulgaria (AP) — Bulgarian maritime authorities on Saturday launched efforts to evacuate the crew of the oil tanker Kairos stranded off the Black Sea port of Ahtopol and believed to be part of the “ shadow fleet ” used by Russia to evade international sanctions linked to its war in Ukraine.

Last week, the Gambian-flagged 274-meter Kairos caught fire after an alleged attack with Ukrainian naval drones in the Black Sea near the Turkish coast. It was sailing empty from Egypt toward the Russian port of Novorossiysk.

The 149,000-ton Kairos, formerly flagged as Panamanian, Greek and Liberian, was built in 2002. It was sanctioned by the EU in July this year, followed by the U.K. and Switzerland.

The ship entered Bulgaria’s territorial waters on Friday under tow by a Turkish vessel, but the mission was abruptly abandoned, leaving the tanker to drift across the sea without power like a ghost ship before stranding less than a nautical mile off the shore.

On Saturday, Rumen Nikolov, in charge of rescue operations at the Bulgarian Maritime Agency, said that it must be established through diplomatic channels why the tanker was brought into Bulgaria’s territorial waters.

Nikolov explained that the empty tanker is stable despite the bad weather, adding that there is no danger to either the crew or the environment. He said that all 10 crew members, of different nationalities, are in good condition and have enough food and water for about three days. “When the weather calms down, the ship will be towed to a safe place,” he added.

The head of border police, Anton Zlatanov, told the Nova TV channel, that communication was established with the crew, who had complied with orders and dropped anchor, and the ship is currently stable in a position off Ahtopol. “The crew expressed their desire to be evacuated, but this must be done in the safest way possible,” Zlatanov added.

Zlatanov noted that the tanker is being monitored by a radio communication system, thermal cameras from the shore, and a radar system, while communication with the crew is being maintained.

Orban to Send a Large Economic Delegation to Russia

In early December, a large business delegation will travel from Hungary to Moscow to engage "exclusively in discussions on economic issues," Hungarian Prime Minister Viktor Orban stated at a campaign rally in the city of Kecskemét on Saturday, December 6. According to him, it is necessary to "start thinking about the world after the war and after sanctions" right now. "We must act proactively because, if God helps us and the war ends without our involvement, and if the American president manages to reintegrate Russia into the world economy and lift the sanctions, we will find ourselves in a completely different economic space," Orban emphasized. He added that he is negotiating with both the U.S. and Russia but cannot "disclose all the details." ## Acquisition of Gas Stations in Europe Hungarian oil and gas company MOL plans to acquire oil refineries and gas stations in Europe owned by Russian companies Lukoil and Gazprom, which are under U.S. sanctions. Additionally, MOL wants to participate in oil production in Kazakhstan and Azerbaijan. Viktor Orban discussed this issue with U.S. President Donald Trump during his visit to Washington in early November, AFP reports. Orban's Visit to Moscow On November 28, the Prime Minister of Hungary visited Moscow, where he met with Russian President Vladimir Putin. Russian participants in the negotiations included presidential aide Yuri Ushakov, Deputy Prime Minister Alexander Novak, and Foreign Minister Sergey Lavrov. This was Orban's second visit to Russia since the beginning of the war in Ukraine. He met with Putin for the 14th time, Reuters reported. In Moscow, Orban promised, among other things, to continue purchasing Russian oil.

https://news.inbox.lv/14zkr56-orban-to-send-a-large-economic-delegation-to-russia?language=en

Dispute centres around sustainability directive that will fine violators