The pork cycle is to economics what the law of gravity is to physics. You can count on it. Every single time. The only thing that makes economics the trickier science, is timing. Because you never know when the market hits peak or bottom. But economics is not an exact science. Investors don't need to get the cycle exactly right to make money. About right cuts it.

The key to understanding the broad commodity cycle, which functions just like the pork cycle, is the time lag between the investment decision and the creation of new supply. What would happen in case there wouldn't be a time lag? An uptick in demand causes a price increase. The price increase causes additional investment. And the surplus demand would immediately be filled by new supply. Same thing on the downside: demand drops, price drops, investment falls, and production would be cut instantaneously. Our hypothetical result: steady prices.

Of course, reality is different. Breeding the hog takes time. When the price of oil or copper rises, companies can probably squeeze out some extra output. But to substantially increase production to fill the new demand, they need to increase exploration budgets. That means hiring new geologists, given that companies probably fired those when prices were low - if they are still around. The geologists need time to search for the treasure. When they find something, engineers need time to figure out how to drill the well or build the mine. Permits need to be arranged. The company might also need to raise capital. And only then, construction would commence.

By the time the whole new enterprise is up and running, demand starts to drop. Due to the price mechanism, users increased efficiency or switched to substitutes. Or a recession hits. At that point, the commodity producers will be holding the bag. And anyone who invested in commodities lately will know exactly what that means.

Our current cycle started in December 2001, when China joined the WTO. That event marked the beginning of the greatest commodity boom the world ever witnessed. The hungry Chinese giant craved commodities. Commodity producers were throwing everything at it, but it never seemed saturated. Then the global financial crisis hit in 2008. After a commodity collapse, prices bounced quickly and forcefully. This strengthened the China hypothesis even further. We were now in a new era.

Except we were not, of course. Multi-billion dollar mines with long lead times came online just as China started slowing down. The law of gravity took commodity prices down to levels not seen since 1974. Continuing our science metaphor, we are witnessing Newton's Third Law applied to economics: the large upward force caused a force equal in magnitude, but opposite in direction. After the Great Boom, we're now in the Great Collapse.

There even seems to be another new paradigm, which is sort of the mirror image of the boom: China switches its economy from industry to services. With the flip of a switch, every factory worker becomes an app developer. Nobody needs stuff anymore, as everything is now 'in the cloud'. China's pace of growth will continue to fall. Commodity prices will extend their tailspin.

Well, maybe the pundits are right. We don't have a crystal ball. But just allow us to add some balancing facts to the China discussion. China is ramping up government spending, just as it did after the financial crisis.

We're not sure how this will end, but the business cycle is also a cycle. China has been slowing down for four years already. No matter what, these measures will provide additional Chinese demand.

Now, more importantly, back to the commodity supply side. The table below shows an extract from a recent Americas Metals & Mining report by Deutsche Bank. Commodity producers are cutting their CAPEX in a huge way. Globally, we see the same picture across the board. That's your pork cycle at work right there. We are once again setting ourselves up for future commodity shortages.

What will cause commodity prices to turn? Well, increased demand and reduced supply of course - nothing new here. But the specifics will be hard to predict. For example, in 2011, nobody was yet aware of fracking. We now know this new technology turned the oil market upside down. There will probably again be some factor we're currently not expecting. An example could be rapidly accelerating growth in India, which is now where China was decades ago. China has 1.36 billion inhabitants. India has 1.25 billion.

It's just a guess. But the commodity cycle will turn. We will know what made it turn only after the fact. But that's not even relevant to you as a shrewd investor. The only thing that matters is that you need to act now if you're serious about making serious money. And gradually expand your exposure to commodities. As the legendary trader Stan Druckenmillernoted:

"The first thing I heard when I got in the business....was bulls make money, bears make money, and pigs get slaughtered. I'm here to tell you I was a pig. And I strongly believe the only way to make long-term returns in our business that are superior is by being a pig."

After what can only be described as a horrific year for metals and bulk commodity prices, market attention is now quickly turning to what the new year will bring.

Some believe that the worst is now over while others think the bear market that has gripped the commodities complex this year is only getting started.

In a note released earlier this week, analysts at Macquarie research have pondered that very question and it doesn’t make for pleasant reading for commodity bulls.

They suggest 2016 will be about the three Ds – destocking, divestment and desperation. Unfortunately for commodity bulls, another D – demand – is unlikely to feature in their opinion. As a result, they’ve made aggressive price downgrades across the vast majority of commodities they cover on the back of “the weaker demand outlook and general cost curve deflation”.

Here’s a snippet from the report explaining their view. Our emphasis is in bold.

For us, 2016 will be the year of the three D’s for commodities: destock, divestment and desperation. Unfortunately not demand, as it is very hard to see where strong, co-ordinated demand acceleration could come from. We are currently projecting 2016 demand for all major metals and bulk commodities remaining well below the 10-year norms. With financial markets taking an increasingly negative view on the long-term health of the industry, pressures on metals and bulk commodity producers seem set to get worse.

In their opinion, the chief cause behind the subdued demand outlook for commodities remains weakness from their largest consumer: China.

The Chinese government used to be like the best company out there – they would give you five-year forward guidance through their five-year plans (backed by a managed political cycle). Now however, the 13th five year plan has little to hang your hat on with few solid targets. Meanwhile, the economy itself has developed a two-speed nature, with the service sector continuing to grow at a fast pace but the old school industrial economy at best stagnating.

This has clearly added to the uncertainty among Chinese commodity consumers, with a knock-on effect back up the chain to producers. Chinese industry, pretty much across all sectors, has built capacity for demand which has not emerged at the same place.

What the researchers at Macquarie are pointing out is that investment decisions from miners and industry made in the past were based on the premise that Chinese demand would continue to grow at astronomical rates for the foreseeable future.

Hopes for a capital expenditure (capex) boom remain on hold.

Morgan Stanley's Capex Plans Index fell to 13.4 in December, the lowest reading since July 2013.

"Continued softness in capex plans echoes the declining trend in capital equipment orders and a heavy inventory correction that has weighed on the manufacturing sector. The effects of dollar strength and uncertainty over falling energy prices have been persistent themes in regional manufacturing surveys in 2015," Morgan Stanley's Ellen Zentner said in a note to clients on Tuesday titled "Damage lingers."

MMM plans for Capex of $1.3-$1.5 billion for 2016 (vs. $1.4-$1.5 billion for 2015)

MMM plans for Capex of $1.3-$1.5 billion for 2016 (vs. $1.4-$1.5 billion for 2015) Bit dated: September polling.

Bit dated: September polling.

Saudi Arabian Oil Minister Ali Al-Naimi said the kingdom, the world's top crude exporter, does not limit its output and has the capacity to meet additional demand, state television Al Ekhbariya reported on Wednesday.

Saudi Arabian Oil Minister Ali Al-Naimi said the kingdom, the world's top crude exporter, does not limit its output and has the capacity to meet additional demand, state television Al Ekhbariya reported on Wednesday.Egypt is going through a foreign currency crisis and is struggling to pay it debts to international trading partners, among them LNG suppliers, Reuters has reported.

The currency crisis follows the blow Egypt suffered following the downing of a Russian jetliner on 31 October when flying over the Sinai Peninsula from the Sharam el Sheikh resort to St. Petersburg, Russia. All 224 onboard the flight were killed. Following the incident, tourism to Sharm el Sheikh suffered a sharp decline as European airlines curtailed flights and governments increased security arrangements. ISIS, the terror group which controls large swathes of Iraq and Syria and has an affiliate organisation in the Sinai Peninsula, claimed responsibility for the attack.

Egypt, according to the Reuters report, is obliged to pay for LNG shipments within 15 days of a shipment's unloading. Now the Egyptian authorities are looking to extend that timeframe. Egypt used to get financial support from the Gulf Cooperation Council (GCC) countries and probably will still get it. However, due to lower energy prices, the support now is more limited. Egypt buys six to eight LNG cargoes monthly, each worth $20-$25 million. It is now in arrears of $350 million for that energy, one source estimated.

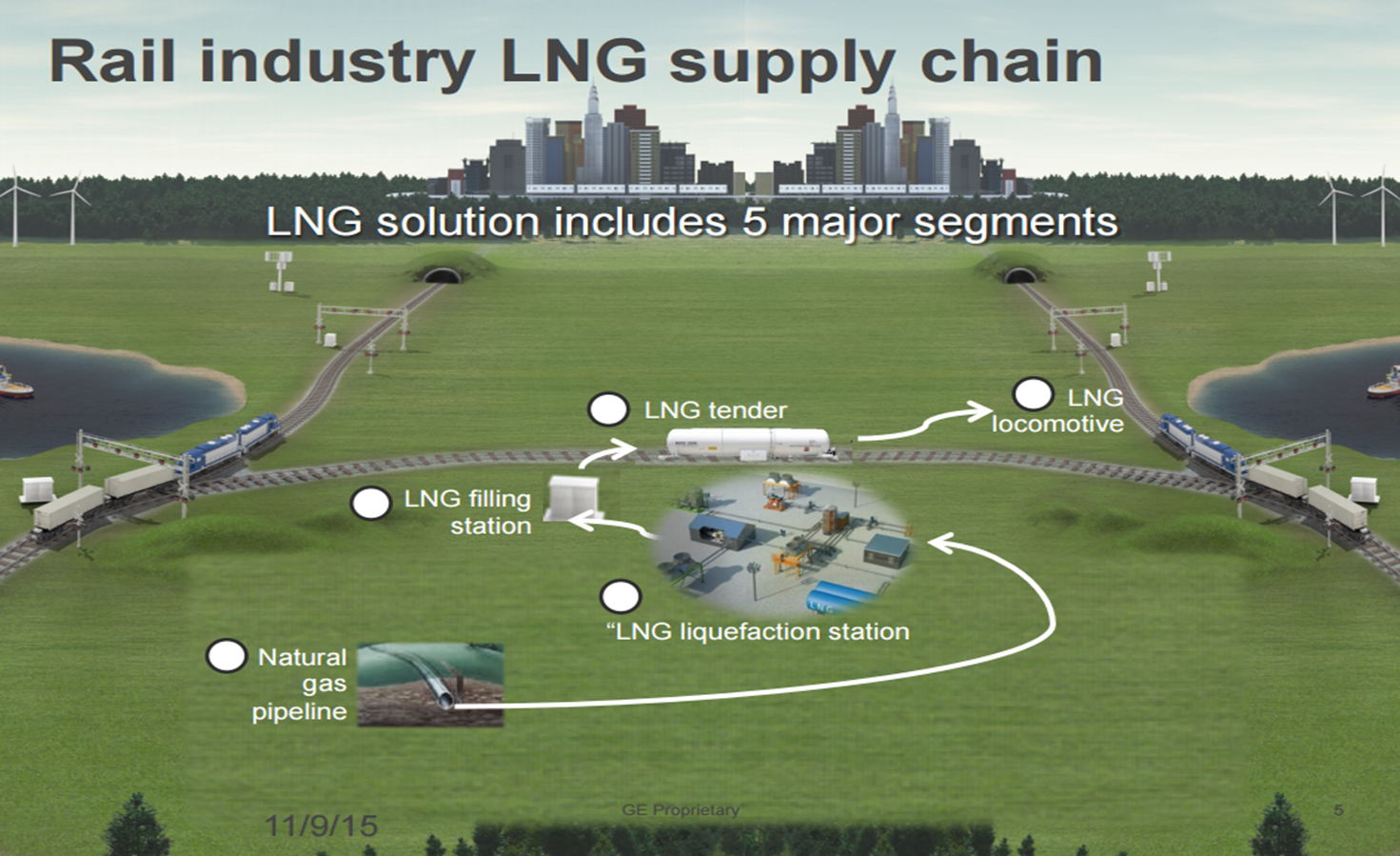

We’ve previously discussed opportunities to use liquified natural gas (LNG) in vehicles including apilot program in the Pittsburgh area for towboats. Ms. Trillanes was able to provide insight into how LNG could be used in our rail systems, including the five major segments required. Her explanation highlights one of the possible benefits of the towboat pilot program: locating an LNG filling station near the rivers would also put it in close proximity to railroad lines in the area.

Please note, all photos below come directly from her presentation and are property of GE Transportation.

Obviously there are several factors to determining if LNG is an economical fuel source for locomotives. The reduced cost of LNG compared to diesel is a driving factor, but operators must also include the cost of operations, training, maintenance and securing a gas supply (or building a filling station).

Another consideration is the replacement rate of diesel by LNG. There are several options when it comes to dual fuel technologies available. Ms. Trillanes explained that GE Transportation had decided the port injection method of using the two fuels as detailed in the chart below.

Currently, GE has three different retrofit kit programs based on the engine technology of the locomotives and they estimate continued testing of the technology in North America throughout 2016.

Activity:

Activity: Inventory:

Inventory: